Cryptocurrency fundamentals

Few facets of the global financial sector and media can escape the growing dialogue and debates surrounding cryptocurrencies. In an increasingly digitalised world, the currencies utilised by consumers are equally susceptible to the effects of the digital revolution. Imagine a purely digital currency with limited to no centralisation of issuing and regulation, a decentralised system of transaction records, and high degree of cryptography employed for the prevention fraud and counterfeiting. Cryptocurrencies are such, threatening to overturn the entire fabric of the existing global financial system and leading the next evolution of market trading.[1]

Cryptocurrencies use Distributed Ledger Technology (DLT) – a decentralised database of multiple managers, the most known being the Blockchain digital ledger. The digital ledgers serve as a repository for all crypto transactions facilitating complete transparency and subsequent accountability, while ensuring against double-spending. The decentralisation of the database enables its self-governance by agents who use and own the specific cryptocurrency.[2] A crucial facilitator to this system is cryptocurrency mining. Miners are responsible for the generation of new crypto coins via the vast decentralised computing networks, and the verification of all transactions recorded on the virtual ledgers.[3] Computers on the network are rewarded with new coins in exchange for the contribution of their increasing extensive processing power.

Emergence and adoption

Prior to the creation of cryptocurrencies such as XRP, Bitcoin (BTC) and the Internet as a whole, purely digital money already existed in experimental and conceptual form, emerging in the late 1990s. Autumn 2008, Satoshi Nakamoto’s white paper titled ‘Bitcoin: A Peer-to-Peer Electronic Cash System’ was published, outlining the function of the Bitcoin Blockchain Network as it came to be known.[4] Nakamoto’s motivations were to catalyse the evolution of a new system that would transcend the inefficiencies of the traditional banking system and enable seamless monetary transactions. It would address the necessity of a centralised authority (government / central banks), the necessity of physical resources, and prevalence of fraudulent activities.

The 2007-08 financial crisis provided the opportune context for such an endeavour, exposing the vulnerabilities and the threat to society and the wider economy of the centralisation of powers within the hands of a few banks and their bad actors. The lines at Northern Rock during the infamous run on the bank epitomises the vulnerability to consumers of the reliance on both physical cash and the traditional banking system. Nakamoto’s creation of the world’s first decentralised was followed by an increasing number of agents within the ecosystem to an extent that investment managers and authors regard cryptocurrencies as a distinct asset class.[5] In 2009, Nakamoto mined the Genesis block, the initial block of the Bitcoin Blockchain igniting a digital currency revolution. The purchase of two pizzas using 10,000 BTC by Laszlo Hanyecz in 2010 saw the earliest real-life BTC transaction, promptly followed by the creation of Bitcoinmarket.com, the world’s first crypto exchange (Prayag, 2019). In just a single year BTC’s priced equalled the US dollar (USD) creating the incentive for the advent of rival cryptocurrencies in the market.

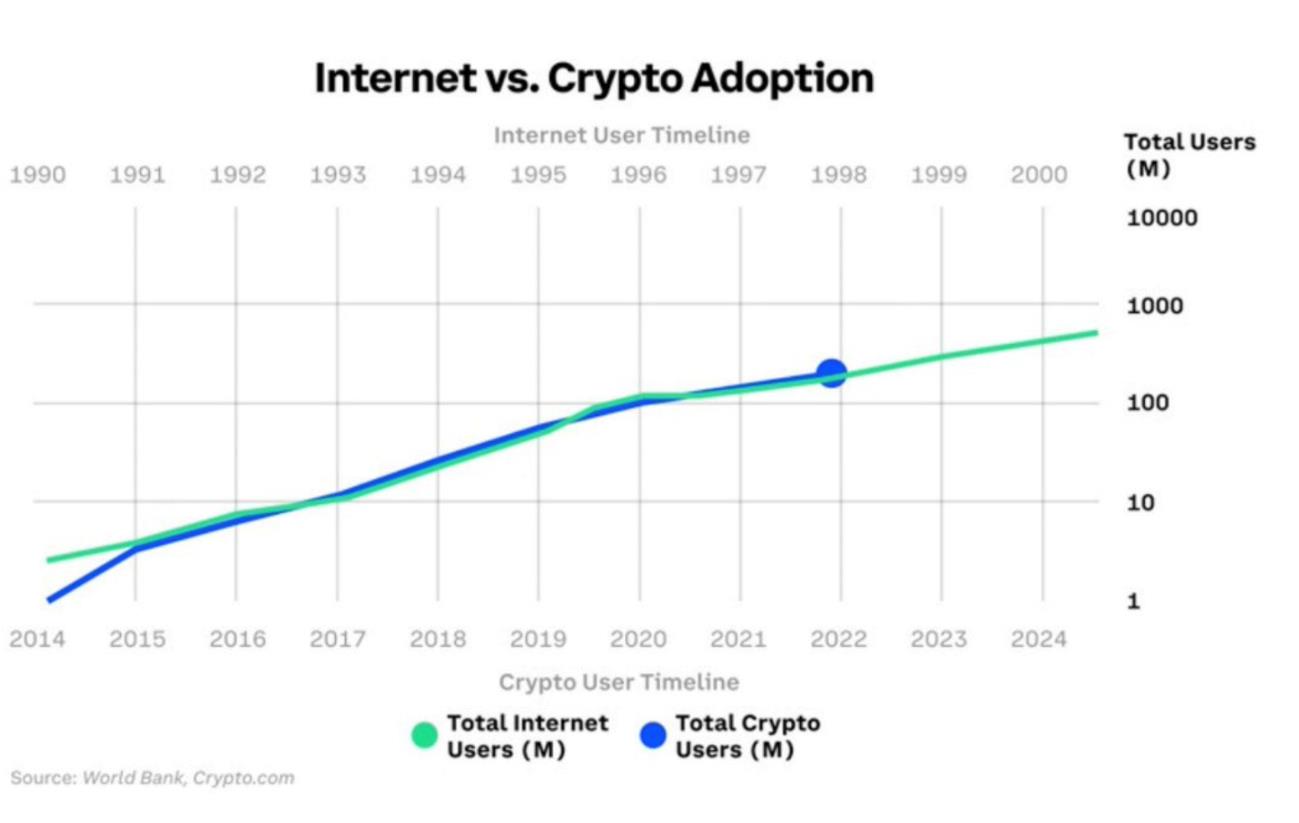

Figure 1: Internet vs crypto adoption

By 2013, Litecoin (LTC) and Ripple (XRP) were among the 10 cryptocurrencies traded in the market. The world’s second largest crypto asset, Ethereum (ETH), was launched in 2015 signalling a tangible explosion in crypto trading with the development of ERC-20 tokens and smart contracts which enable the verification and enforcement of transactions/contracts without the need for third party involvement, thus being of incredible utility. ERC-20 serves as the Ethereum Blockchain standard for smart contracts creation and issuing.

A further development of the crypto market was the first Initial Coin Offering (ICO) in 2015, the crypto-world equivalent of an Initial Public Offering (IPO). The Augur Digital Asset ICO offered an ERC-token on the ETH’s smart contract network. To date, BTC and ETH retain their dominance of the crypto market via market capitalisation, with a further 2700+ crypto assets now trading on the market. Understandably, the rate of adoption of cryptocurrencies correspond to that of the internet and the technological development of the necessary computing and software capabilities, illustrated by Figure 1 above. As computing technologies such as quantum computing advance, one can hypothesis the equal expansion of the crypto economy. Another conspicuous development the increasing discovery of real-world uses of cryptocurrencies – from financing revolutions, fundraising to online shopping, the uses of cryptocurrencies seem virtually limitless.

Benefits of cryptocurrencies

In 2021, A Hoover Institute Policy Seminar in Basel, Switzerland explored the dynamics of digital currencies and the future of the international monetary system. Remarks by Agustin Carstens, General Manager for the Bank of International Settlements (BIS), during this seminar elucidates the role of digital currencies as the next evolution of Real-time Gross Settlement (RTGS) systems. Carsten additionally outlines the choice facing society of adopting of a purely decentralised system vs one with a central authority.

Should society choose to adopt a purely decentralised system in the spirit of Nakamoto, this would ensure several benefits. On the macro level, the decentralised paradigm represented by cryptocurrencies eliminates a single point of failure leading to a widespread financial crisis such as the collapse of Lehman Brothers, as such this in theory creates a more stable financial environment. With the subsequent effects of the 2008 financial crisis (austerity, social unrest, anti-globalisation populist movements and so on), there is increasing appetite to erect a system that would prevent a repeat of such an occurrence.

On the micro level, cryptocurrencies are posited as ensuring easier direct transfers of funds between parties within ultra-secure systems. The lack of an intermediary makes these direct transfers occur faster in comparison to traditional money transfers. Within Decentralised Finance (DeFi), flash loans exemplify the speed of these transactions. The loans are executed within seconds for immediate use in trading without the need for collateral. The ease of use for individual parties is mirrored by the evident profit potential of cryptocurrencies for investors via its streamlining effects on the money transfer system.

Drawbacks of cryptocurrencies

With the above benefits, there are equally potential vulnerabilities of cryptocurrencies. It is virtually impossible to determine the fair value of these assets due to their novel and intangible nature, which creates an environment conducive to speculation.[6] This makes it difficult for investors to generate stable returns and limits their potential as diversification assets for fixed income, equity, and commodities.[7]

Furthermore, cryptocurrencies are theoretically decentralised with distribute wealth across multiple parties, yet an MIT study found that 45% of BTC was held by just 11,000 investors, indicating a concentration of ownership equally found in the traditional financial system (Markarov and Schoar, 2021). This is amplified by the high capital and energy costs for mining cryptocurrencies which serve as a barrier of entry though in theory anyone can mine them.[8]

Additionally, cryptocurrencies can also be deployed effectively for illicit or nefarious uses such as money laundering as in the case of Dread Pirate Roberts, a case study of the utilisation of cryptocurrency for the sale of drugs on the dark web. Though posited to be highly secure, the underlying non-blockchain systems are susceptible to hacking resulting in millions (USD) worth of crypto coins being stolen. The potential for losses also crosses over into the investment dynamics of cryptocurrencies. Publicly traded crypto assets are vulnerable to high degree of volatility as in the case of BTC which experiences rapid surges and crashes in value, leading some economists to describe cryptocurrencies as a speculative bubble (Redman, 2019).

Research aims and objectives

The following research explores the stability of the DAI stablecoin. There are four study questions that are concentrated on the stability of the DAI:

- What is the level of stability of DAI using Dynamic Conditional Variance (DCV)?

- What is the most ideal cryptocurrency collateral for DAI using Dynamic Conditional Correlation (DCC)?

- In comparison to other cryptocurrencies, can the DAI stable coin be considered a diversifier, hedge, or haven?

- Can DAI be regarded as a risk-free asset within a portfolio?

CoinCapMarket.com and Yahoo Finance were consulted for this data collection. Due to the recent emergence of the stablecoin market as well as the constraints imposed by the data retrieval panels, the research was conducted across a period that included a span of two years. As the sample data for this study, we have retrieved the open price, closing price, adjusted price, and market capital of Ether (ETH), USD coin (USDC), Basic Attention Token (BAT), Bitcoin (BTC), Maker (MKR), and Tether (USDT). These cryptocurrencies are represented by the letters ETH, USDC, BAT, BTC, and MKR respectively. However, because of the unique characteristics of stablecoins, the logarithm of the daily return of the sample data was used in this investigation so that the data could be presented in a manner that was more like that of a normal distribution.

Conclusion

This study investigated the stability of DAI stablecoin, namely, whether, stablecoin is stable or not, and which cryptocurrency is suitable to be used as collateral of DAI stablecoin. I have also investigated the diversifier, hedge, and safe haven features of DAI stablecoin against ETH, USDC, BAT, BTC, MKR, and USDT, in which ETH, USDC, and BAT are the commonly used collateral of DAI, while the other cryptocurrencies are not, but still very commonly used collateral in the cryptocurrency market.

Because of the pegging feature of DAI stablecoin, the price changes of DAI might not be easily observed, so throughout the study, I chose to use the logarithm of the daily return of the closing price of DAI stablecoin instead of the daily closing price.

I first used a standard GARCH model (sGARCH), and exponential GARCH model (eGARCH) to investigate whether DAI is stable or not in the market. Then I employed the DCC-GARCH model to gather the dynamic conditional correlations between the DAI stablecoin and other sample cryptocurrencies. I then established dummy variables for extreme movements in the falling market to build dummy variable regressions to examine the potential properties of DAI stablecoin against all the other sample cryptocurrencies. The data was analysed during a two-year time window between 1 January 2020, and 31 December 2021, however, due to the lack of data, there was only one year's data for MKR. To test the loss-reduction abilities of stablecoins from a risk management perspective, I calculated VaR and ES reductions, defined as the differences between VaR and ES of portfolios which contains DAI stablecoin and other sample cryptocurrencies, respectively.

There are four major findings of this study.

- By looking at the presentation of the sGARCH and eGARCH results, the volatility presented a flat shape, which means that DAI is performing very stably in the past two years.

- The shape of the volatility test results of DAI stablecoin matches the shape of the volatility test result of the US dollar index consistently. They both present high volatile tendency at the end of the fiscal year 2021, which means the stability of DAI stablecoin is highly related with the value of the US dollar.

- Based on the dummy variable regression, I found that DAI stablecoin functions very well as a safe haven against cryptocurrencies with the same pegging policy. However, for the rest of the cryptocurrencies, DAI functions as a weak safe haven against them. Also, DAI stablecoin can function as a very good diversifier against most of the cryptocurrencies except for Tether. The result shows that DAI is a strong hedge against Tether, therefore, in the analysis during the two-year window, DAI presented with high quality properties against other stablecoin and traditional cryptocurrencies. Thus, Tether and USD coin can collaborate very well with the DAI stablecoin, and they can be very good collaterals for the DAI stablecoin to be minted.

- From the risk management perspective, it is found that DAI has a very stable feature to be kept in the portfolio, because the downside risk for DAI to be in the portfolio with any of the sample cryptocurrency is very low. Besides, comparatively, the portfolio which contains Tether and USDC are even more stable, as their VaR and ES in all the extreme quantiles are the lowest, indicating that DAI stablecoin can be regarded as a great tool in reducing extreme losses. Nevertheless, the results of the risk management test are highly consistent with the dummy variable regression tests, which elaborates that Tether and USD coin are qualified backups for DAI stablecoin users.

References

[1] Lansky, Jan. 2018. 'Possible state approaches to cryptocurrencies', Journal of Systems Integration 9: pp.19–31.

[2] Corbet, S., Meegan, A., Larkin, C., Lucey, B. and Yarovaya, L. (2018), ‘Exploring the dynamic relationships between cryptocurrencies and other financial assets’, Economics Letters 165, pp.28–34.

[3] Li, R., Sufang, L., Di, Y., and Huiming, Z. 2021. 'Investor attention and cryptocurrency: Evidence from wavelet-based quantile Granger causality analysis', Research in International Business and Finance 56: 101389.

[4] Nakamoto, S. 2008. Bitcoin: A peer-to-peer electronic cash system.

[5] Glaser, F., Zimmermann, K., Haferkorn, M., Weber, M. C. and Siering, M. 2014. ‘Bitcoin-asset or currency? Revealing users’ hidden intentions’, Revealing Users’ Hidden Intentions (April 15, 2014). ECIS.

Phillip, A., Chan, J. S. and Peiris, S. 2018. ‘A new look at cryptocurrencies’, Economics Letters 163, pp.6–9.

Corbet et al., 2018.

Gil-Alana, L.A., Abakah, E.J.A. and Rojo, M.F.R. 2020. ‘Cryptocurrencies and stock market indices. are they related?’, Research in International Business and Finance 51, p.101063.

Sifat, I. 2021. ‘On cryptocurrencies as an independent asset class: Long-horizon and covid-19 pandemic era decoupling from global sentiments’, Finance Research Letters p.102013.

[6] Fry, J. and Cheah, E.-T. 2016. ‘Negative bubbles and shocks in cryptocurrency markets’, International Review of Financial Analysis 47, 343–352.

Huynh, T. L. D., Nguyen, S. P. and Duong, D. 2018. 'Contagion risk measured by return among cryptocurrencies', in International econometric conference of Vietnam, Springer, pp.987–998.

Baur, D. G. and Dimpfl, T. 2018. ‘Asymmetric volatility in cryptocurrencies’, Economics Letters 173, pp.148–151.

Vidal-Tomás, D., Ibáñez, A. M. and Farinós, J. E. 2019. ‘Herding in the cryptocurrency market: Cssd and csad approaches’, Finance Research Letters 30, pp.181–186.

Kaiser, L. and Stöckl, S. 2020. ‘Cryptocurrencies: Herding and the transfer currency’, Finance Research Letters 33, 101214.

Fruehwirt, W., Hochfilzer, L., Weydemann, L. and Roberts, S. 2021. ‘Cumulation, crash, coherency: A cryptocurrency bubble wavelet analysis’, Finance Research Letters 40, 101668.

[7] Yermack, D. (2015), Is bitcoin a real currency? an economic appraisal, in Handbook of digital currency, Elsevier, pp.31–43.

[8] Mba, J.C., Edson, P., and Ur, K. 2018. 'A differential evolution copula-based approach for a multi-period cryptocurrency portfolio optimization', Financial Markets and Portfolio Management 32: pp.399–418.

Mba, J.C, and Sutene, M. 2020. 'A Markov-switching COGARCH approach to cryptocurrency portfolio selection and optimization', Financial Markets and Portfolio Management 34: pp.199–214.

10 November 2022